The winners and losers of the automotive industry paradigm change

I've been discussing the automotive market for years here as (a) it's a fascinating mix of economic pressure meets technology disruption meets consumer behavior change meets geopolitical turmoil, and (b) I do work for various operators of this market ranging from startups trying to disrupt par to it, to automakers themselves.

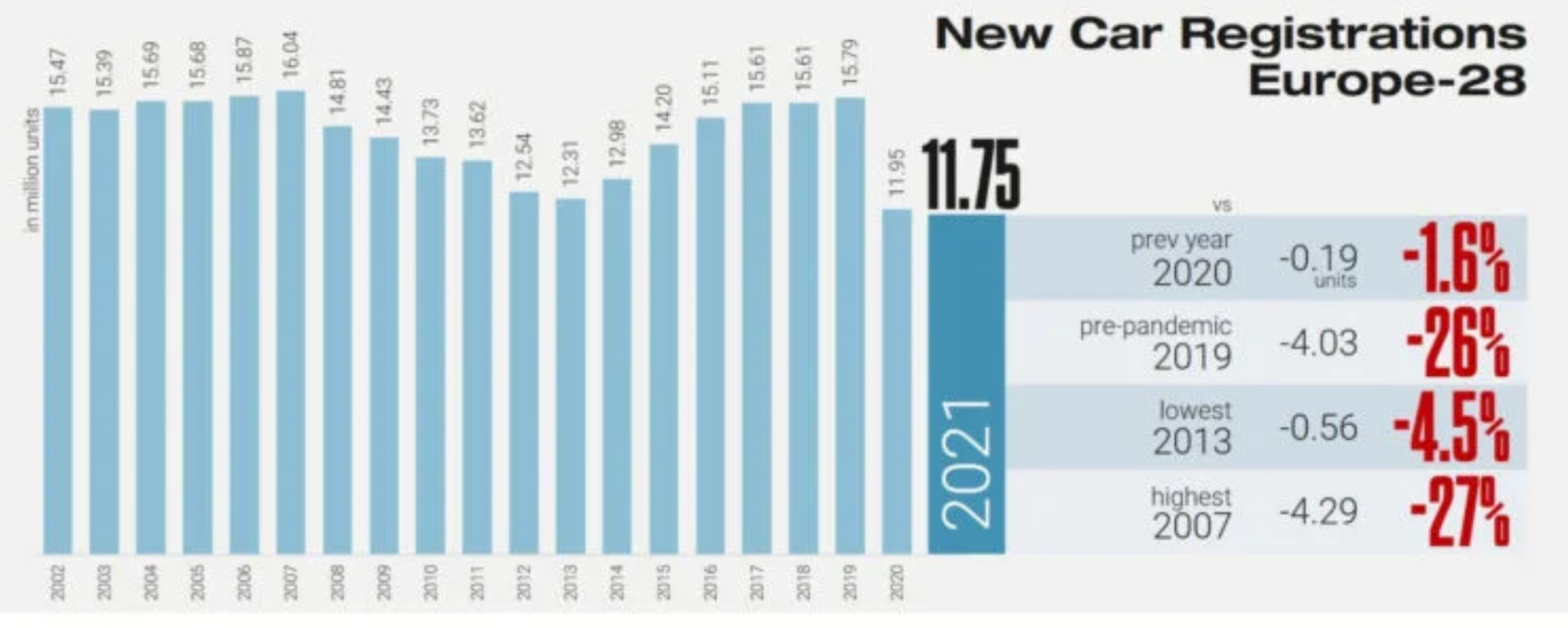

What is most fascinating is certainly how the innovator's dilemma has been playing by the book without missing a step for incumbent automakers in the U.S. and Europe. As a highly capitalistic market that is also extremely demand-constrained and running on razor-thin margins, no surprise that incumbents are at a tremendous disadvantage when facing major technological transitions.

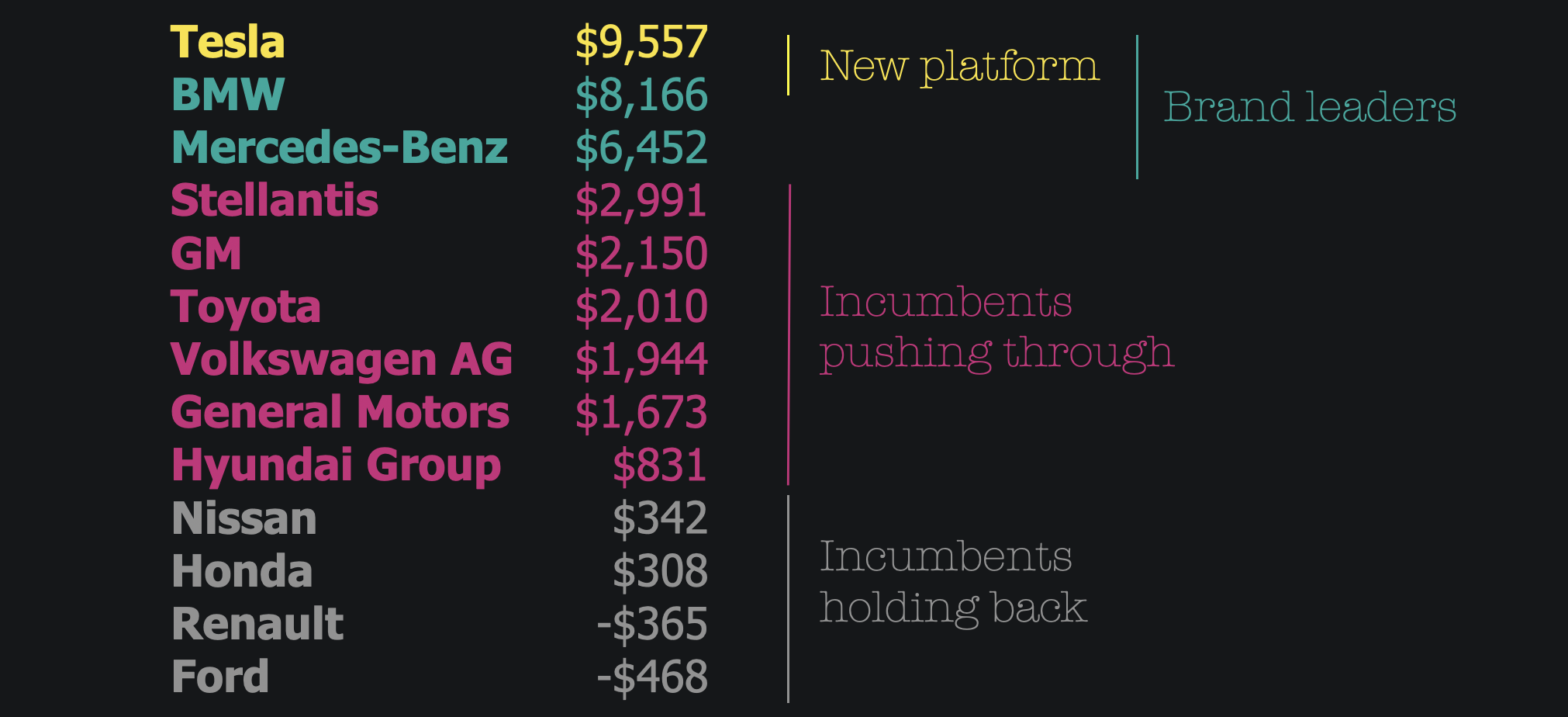

And suppose you only consider the margin advantage. In that case, you have a picture showing the new automotive platforms head and shoulders above everyone else (mainly Tesla mainly for now, but not for too long), German brand leaders that still command a premium on the market with mostly old engine platforms, a cohort of incumbents that started to invest late in the game in EVs that are struggling with margins but clawing back, and finally a long tail of incumbents that struggle both on their brand value and on their investments to jump back in the new EV market:

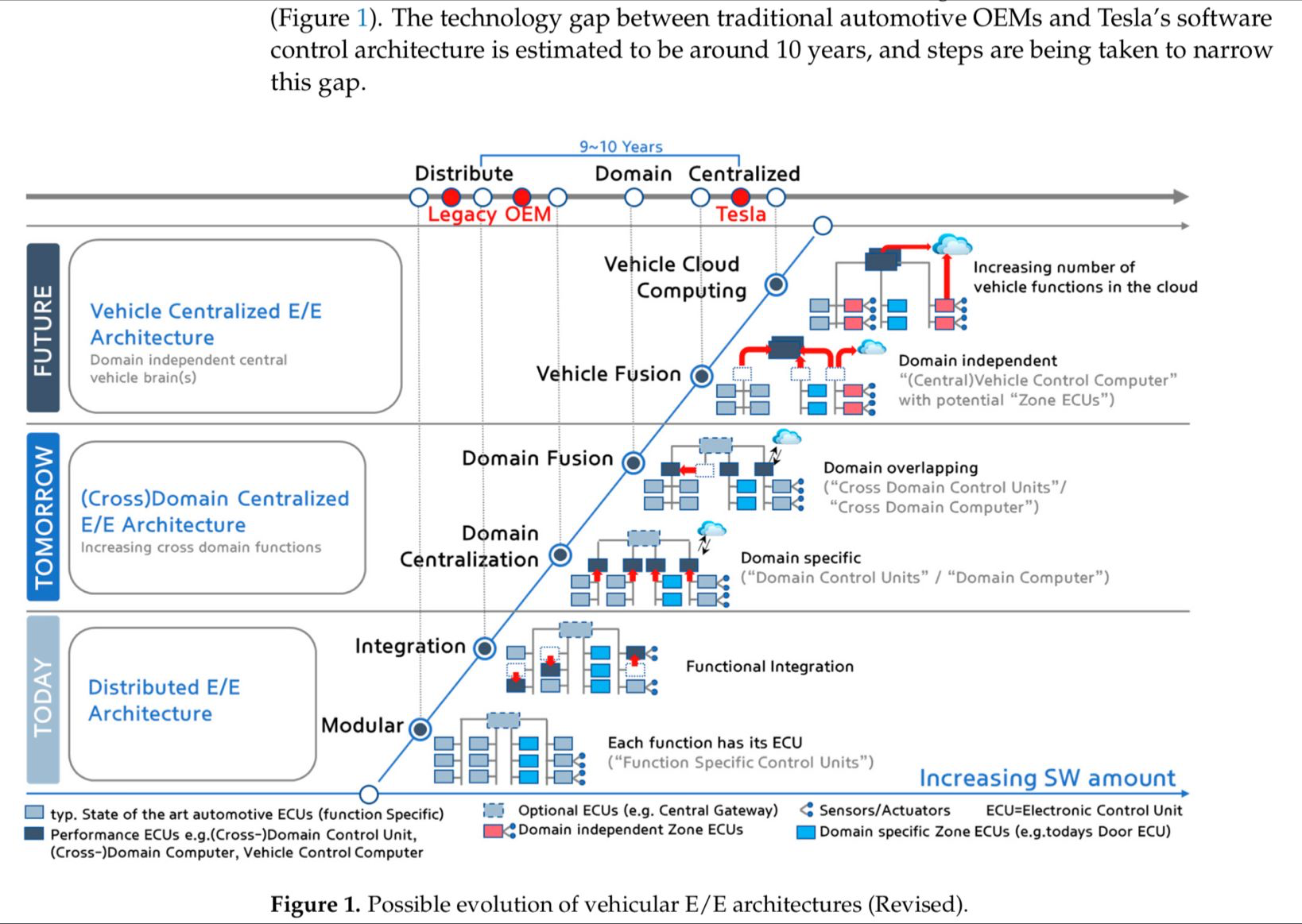

The real competitive advantage in this market is still held by Tesla, which, unbothered by legacy systems, has developed a tremendous competitive advantage on electric power trains, batteries, security systems, and software. A recent McKinsey study of OEMs in the car industry pins Tesla 10 years ahead of the rest of the market (this obviously makes for a good title and might not mean much, but still):

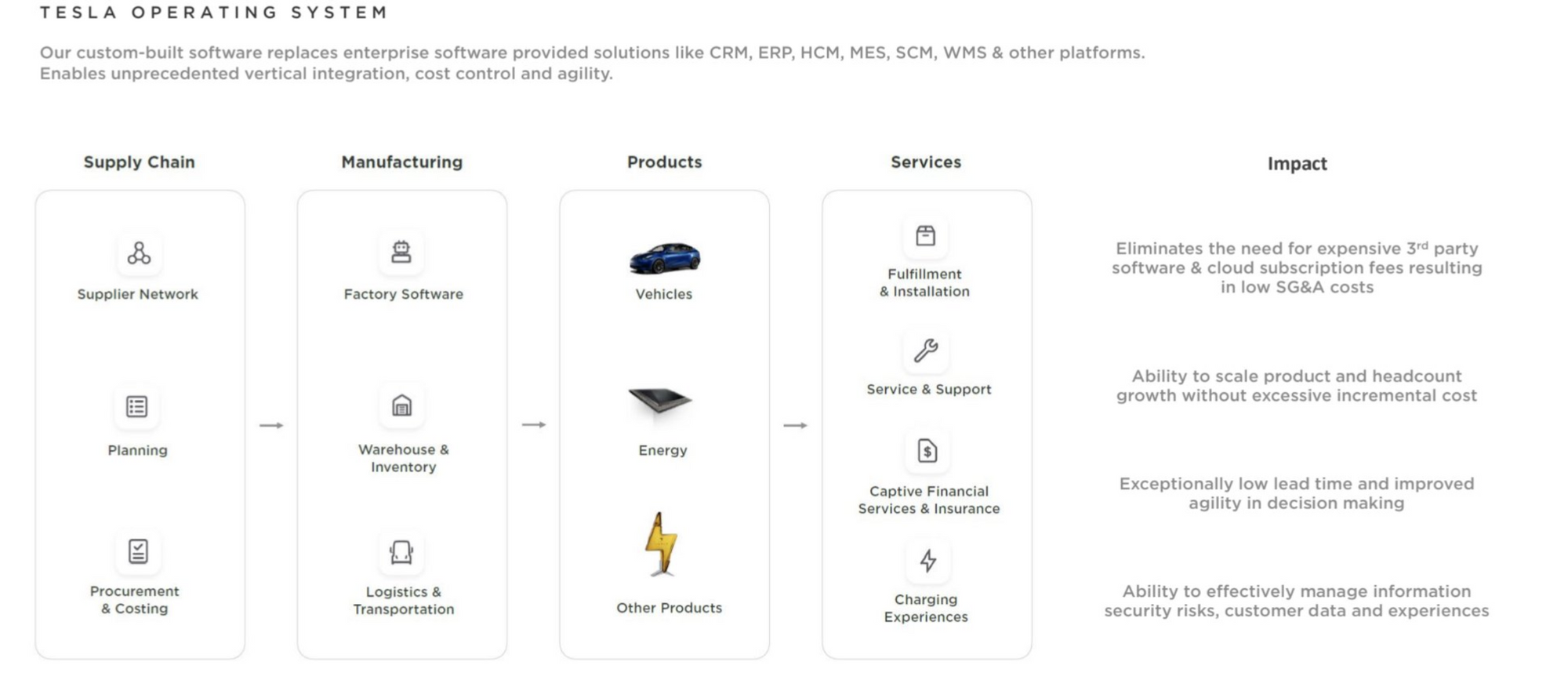

The irony, of course, is that traditional car companies mostly saw software as hidden and deeply technical security features with a layer of an entertainment system. And they are still mostly happy to let others care for the latter. Meanwhile, beyond, the software aspect, Tesla doesn't even think of itself so much as a car company but rather as a full-on operating system for electric mobility:

Or, as I often write about, Tesla is more an energy than a car company... which becomes quite confusing for analysts that only factor in 'cars' as the stock keeping unit of this business:

Not to mention the confusion of the rest of the industry that does try to understand how being a platform works and clumsily tries to create recurring revenues around seat heating or in-car entertainment:

In this game, Tesla still has the lead as a digital-native company that also can pivot its platform business to adjacent markets, such as supply chain:

And in the West, after more than ten years of constant push, Tesla is also an interesting proxy to measure how far each country is in transitioning to EVs. As I was writing back last November, "What is rather amazing to me is that the EV paradigm has now fully entered early core market mode. The electrification of the car is not an "if?" or a "when?" but a "how far?"

But the last, and certainly deadliest, factor to consider is the fast arrival of Chinese manufacturers that mostly rebooted their car industry to full electric, with massive investments in battery manufacturing. Which, for Europe (and to some extent the U.S. as well), is a major bottleneck:

For those who have followed this market for the last ten years, there should be zero surprises to now see the Chinese BYD automaker smoothly entering the European market with a Tesla-like master plan. Except that, if Tesla still can't sell cars (or doesn't want to) below the €50K mark, BYD is already there:

When I say that this market has certainly become the mother of all innovator's dilemma cases, I'm not exaggerating one bit:

And the next step will be another business school's favorite concept: full-on disruption (*) with Chinese vehicles entering the European market at a jaw-dropping €10,000 price point.

Dan Mihalascu

Dan Mihalascu

What is still vastly misunderstood is that such a disruption is not just a race to the bottom on price with low-quality vehicles but a systemic paradigm change in how such vehicles are designed, manufactured, financed, delivered, and serviced globally. While Europe is still thinking about building cars, the rest of the world has started to shift its mindset and think in terms of platforms entirely.

And this started ten years ago...

Ruptures are always slow in the making, and then, seemingly overnight, they become the new paradigm. This is true for the automobile market just as it's true for your own market, whether you are in retail luxury, defense systems, or B2B SaaS platforms...

(*) For reference: