Wide vs Deep, the margin strategy of innovators

For years, Apple has been vastly underrated in many sectors, such as mobile or games, and now as an ad or financial service company. Mostly the reason is that Apple until it's late in the game, doesn't game a significant market share. Their focus is never on eating the most cake but on taking the tastiest bite.

For instance, most analysts wouldn't classify Apple as a game company. Their focus is not on being a gaming company; their revenues in gaming are not that significant compared to the likes of Microsoft, Activision Blizzard, Sony, or Nintendo. Just one thing, though, since 2019, Apple's profits in games are above the combined profits of all the previous companies I've just cited. Not a game company, you said?

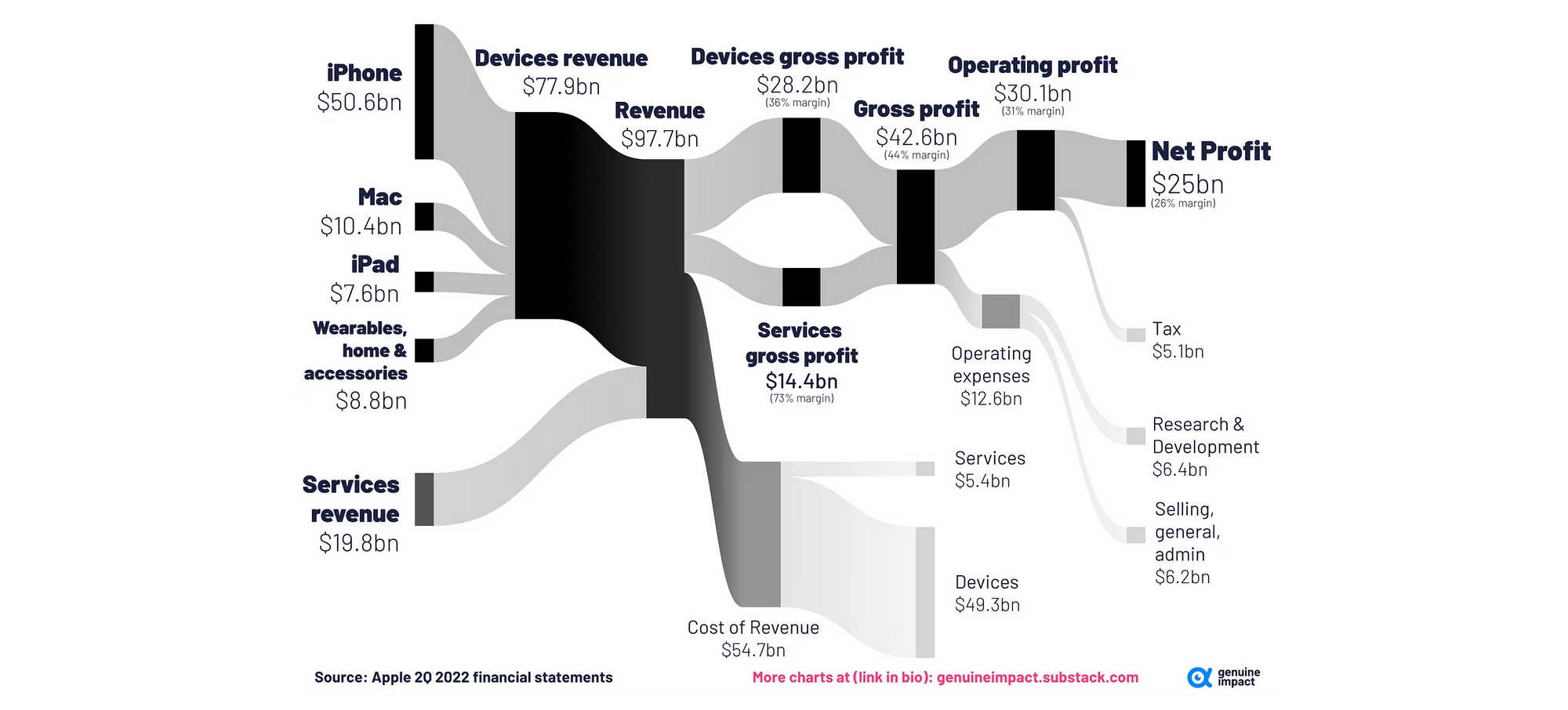

Their latest Q2, 2022 financial statement report is quite interesting too. With a 31% operating margin and a net profit margin of 26%, they have hyper-contributors such as their services with a mind-boggling 73% gross margin 🤯

As we already discussed, reading the market through size in revenues can be deceptive and, quite frankly, a rookie mistake. Size matters, yes, if you're measuring the money that stays within the company to fuel further R&D, marketing, innovation, and new product lines.

Apple's margin strategy is always the same, starting as a niche player and focusing on margin growth while keeping operating expenses and costs of revenue as tight as possible. They grow deep, not wide, if you will.

Which, as a side note, is a key argument to bet against an Apple car (why go from a 57% gross margin business to a 7% gross margin market?).

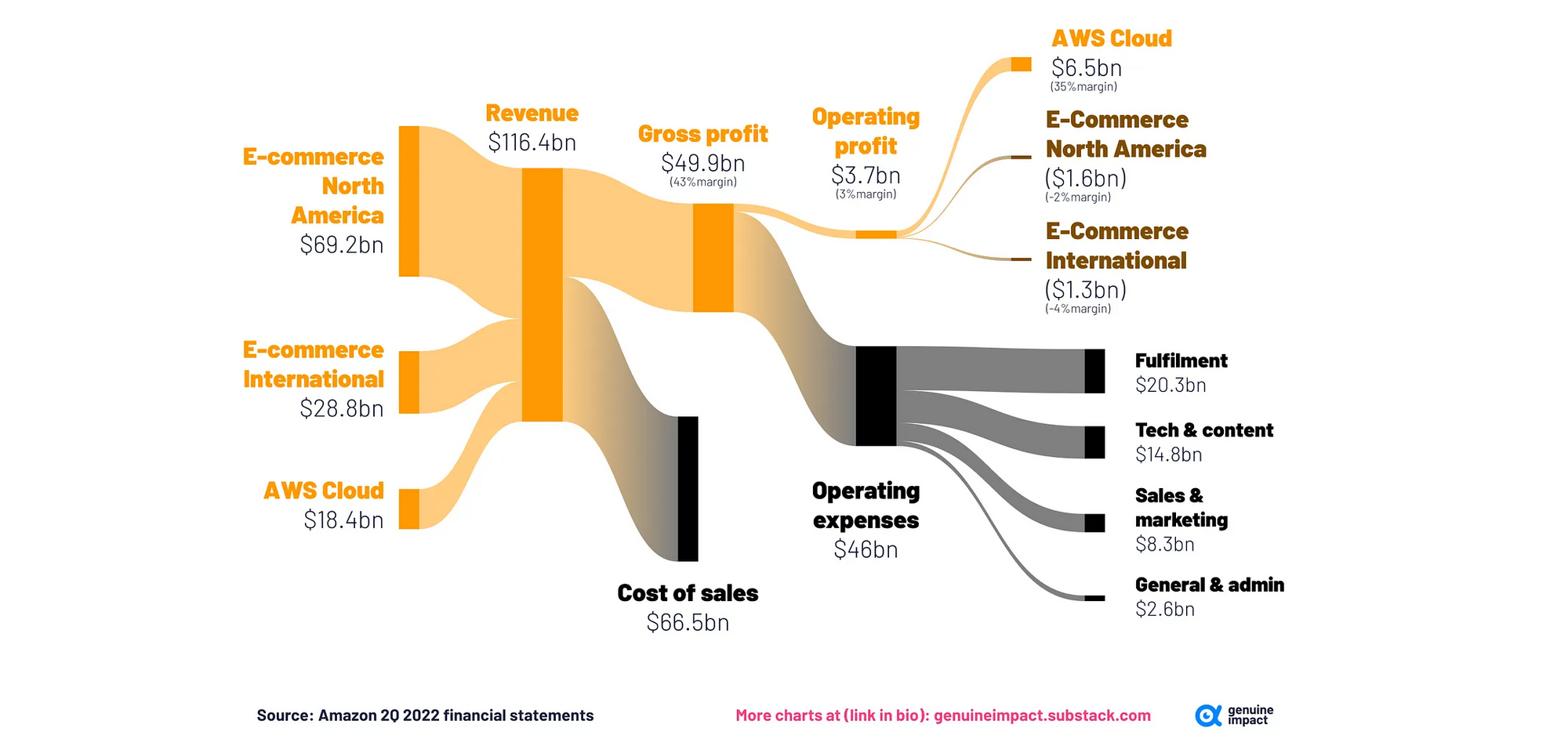

Amazon is another fascinating company with a particular margin strategy. While Apple is always going deep (profits), Amazon has had to deploy and sustain one of the largest network effect businesses worldwide since 2007. They had to go not only wide but exponentially wide (sales expansion prevailing on pretty much anything else).

After leveraging cheap capital investment for years, Bezos' genius stroke was to create AWS (Amazon Web Services) as a highly profitable stand-alone service. AWS started as a way to monetize the extra computing capabilities of Amazon's e-commerce infrastructure. This is what is still allowing Amazon e-commerce to go wide with low margins while AWS is going deep, fueling juicy margins in the joint financial structure.

By the way, this wide + deep strategy is so powerful that it's center-stage for anyone making the case that Amazon is having anticompetitive behavior in the e-commerce sector by running at losses their mega-platform.

Why do I write about this?

As I briefly mentioned in another article, sales are a vanity metric. They don't tell the real story of a business.

And when innovating, companies are mostly rushing for a land grab, trying to make their first sales in a new market without thinking about profitability so much to begin with. While this can make sense, it's the least good strategy most of the time.

Suppose you're trying to enter (or create) a new market instead of playing wide for scraps. In that case, the common sense should be to go deep into your initial core market (even if it's a niche) and assess that these customers are ready to pay a premium to eliminate an acute pain. Expanding further out your innovation formulation to adjacent customers less in pain will mean going wider but with less margin. And this is not a fatality; it's a choice.

Unless, like Amazon, you're a pure platform business that will live or die by network effects.