🟢 Building a proper innovation portfolio - Part 2

In this second part of our series on how to build a proper corporate innovation portfolio, we are talking numbers, critical mass of projects, and optionality over serendipity!

Part 1 quick recap

In Part 1 of this series, we discussed how innovation is a non-linear game not well served by the usual project pipelines.

We presented the core framework of a portfolio strategy that we've been using for years in industries going from aerospace to beauty products. It's a two-dimensional exploration map dealing with different levels of market/technology uncertainties. And we went around the different logics and ROIs involved in the New Frontier, Business Transition, and Beachhead to the Core Market zones.

We also started to discuss that as soon as you grasp the non-linear aspect of innovation, you understand that you won't be able to outsmart all uncertainties of the market. Trying to predict what project to bet on to deliver an innovation three or five years from now is a recipe for disaster.

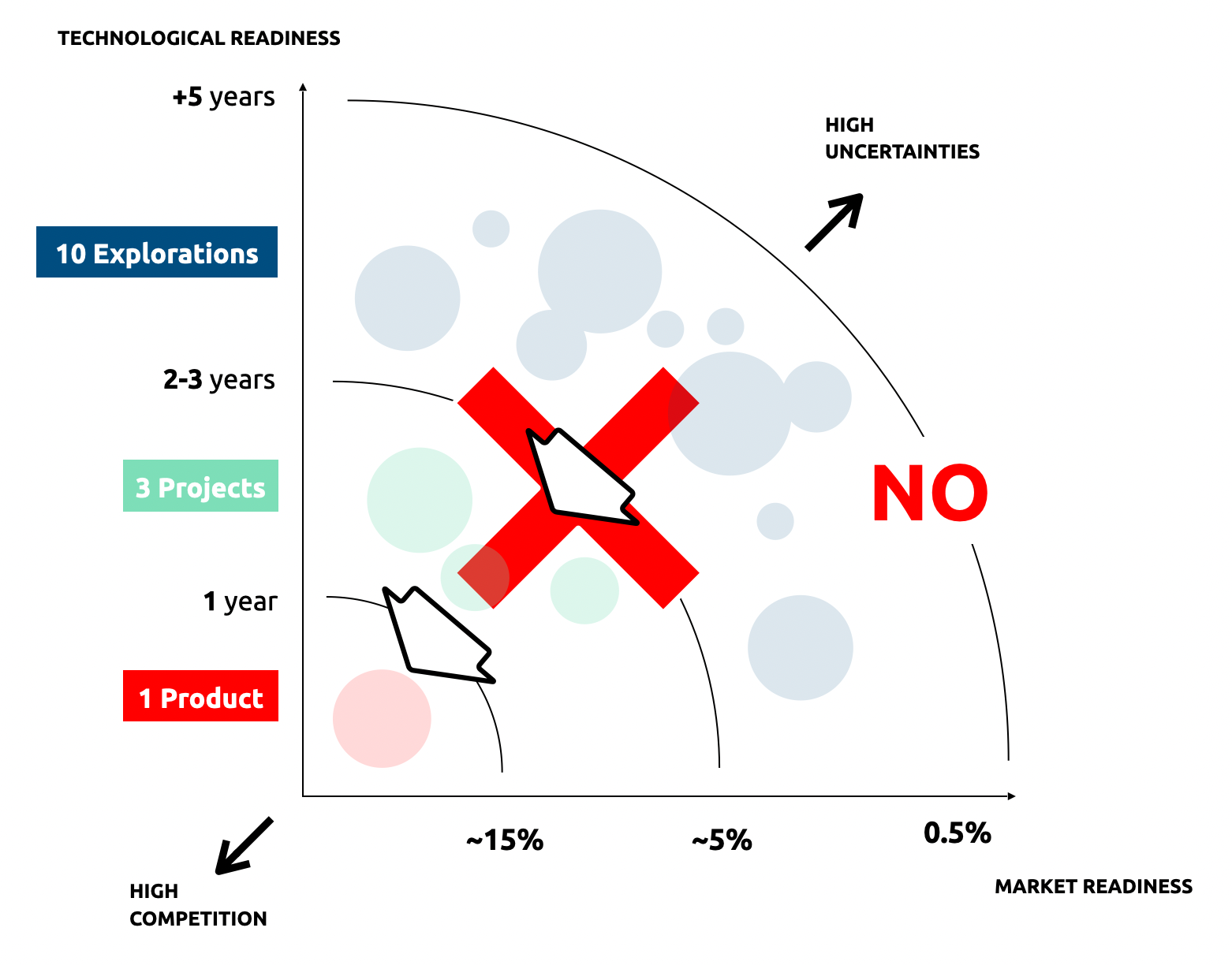

Really, it's not a pipeline!

The core difficulty when discussing an innovation portfolio is that your brain still thinks pipeline. Always. And for instance, regarding what we discussed last week, you are still probably thinking like this...

I am not saying that some projects explored in the high uncertainties zone won't mature and sometimes graduate to fully-fledged products. I am saying it's not the rule.

The reason should be obvious: the higher the uncertainties you are working on, the higher the failure rate of individual projects. Whether you run them internally through an entrepreneurship program or externally with open innovation doesn't matter much.

If you expect a 90% failure rate in the highest zone of your portfolio, about 50% in the middle zone, and only 10% in the bottom zone close to the core market offers, it's easy to do the maths and understand you'll never pipeline successful projects out of this. You will wait for three years to realize that the projects you pushed in your pipeline don't deliver any ROI.

Intermediate ROIs are key

The mindset shift you need to operate is to be way more aggressive with your ROI expectations. Instead of pushing ideas in a pipeline and waiting for an elusive success, ask yourself how you can deliver monthly ROIs and, down the road, make sure you'll have a major success or two to cash in your core market.

To build upon what we already discussed last week, this is how you make it work:

The proper mindset here is:

- Accept unavoidable failure of individual projects (we'll elaborate more on this).

- Make sure to get ROI out of each project but understand that most of them won't be strictly "new businesses" but more intermediate and yet highly valuable ones.

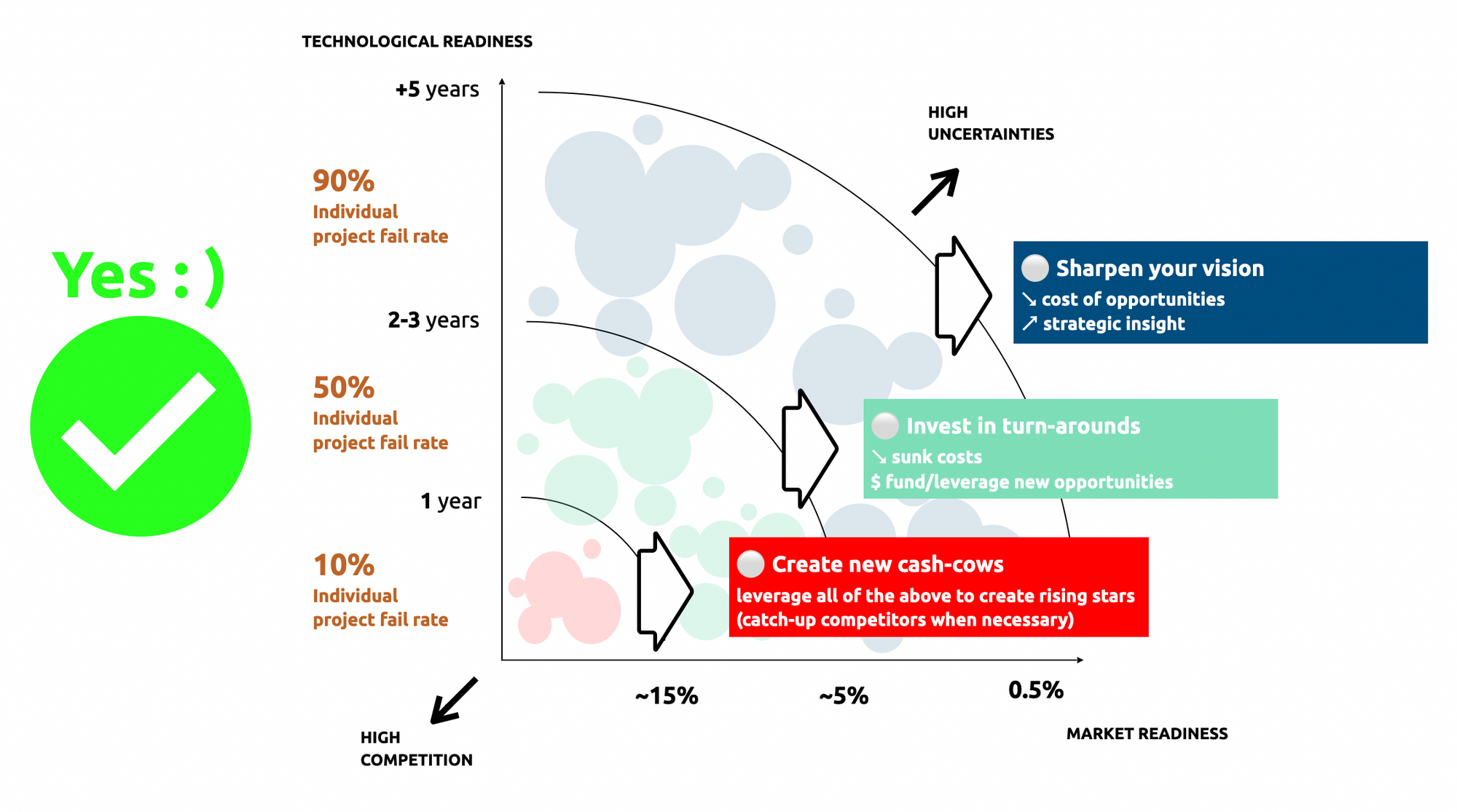

- Adjust your expectations to each zone of the portfolio. The more uncertainties, the more strategic your perspective should be. The fewer uncertainties (and more competition already), the more it's about time-to-market.

Again, another way to explain it is that each zone of your innovation portfolio should be treated as a different type of profit center. In high uncertainty zones, the 'profit' is strategic acumen; down close to your core market, it's about the speed of delivery.

For example, if you invest in an artificial intelligence startup with your open innovation department that develops highly accurate consumers forecast, you're betting on a highly uncertain technology. Your failure rate on such projects will be around 90%. That's fine; now that we know you will not make money directly with this, what are the real ROIs you should seek? Understanding why these models still don't work to know what will unlock them and be prepared to come back more aggressively to this tech? Detect new talents working on AI that you could recruit to dramatically increase your operational excellence on a current product line? Discover that a simpler technology is still beating AI prediction in your field, and you should not disinvest from it yet? The answer to all these options is YES.

All these intermediate ROIs potentially deliver a tremendous amount of cash-on-cash returns. It's just a matter of not getting caught in your own hype on the initial projects. The value is aggregated from the whole portfolio, not a single project.

Size does matter

Until now, I've danced around a key question: how many projects do we need to build such a portfolio?

To answer this question, what can use a simple proxy: thirty years of modern venture capital firms and angel investors' track records (or lack thereof). When considering smart investors working full-time on detecting the best of the best startups and the limit they have at this game, success appears when reaching a critical portfolio size.

Being smart can only get you that far when dealing with innovation; you need volume.

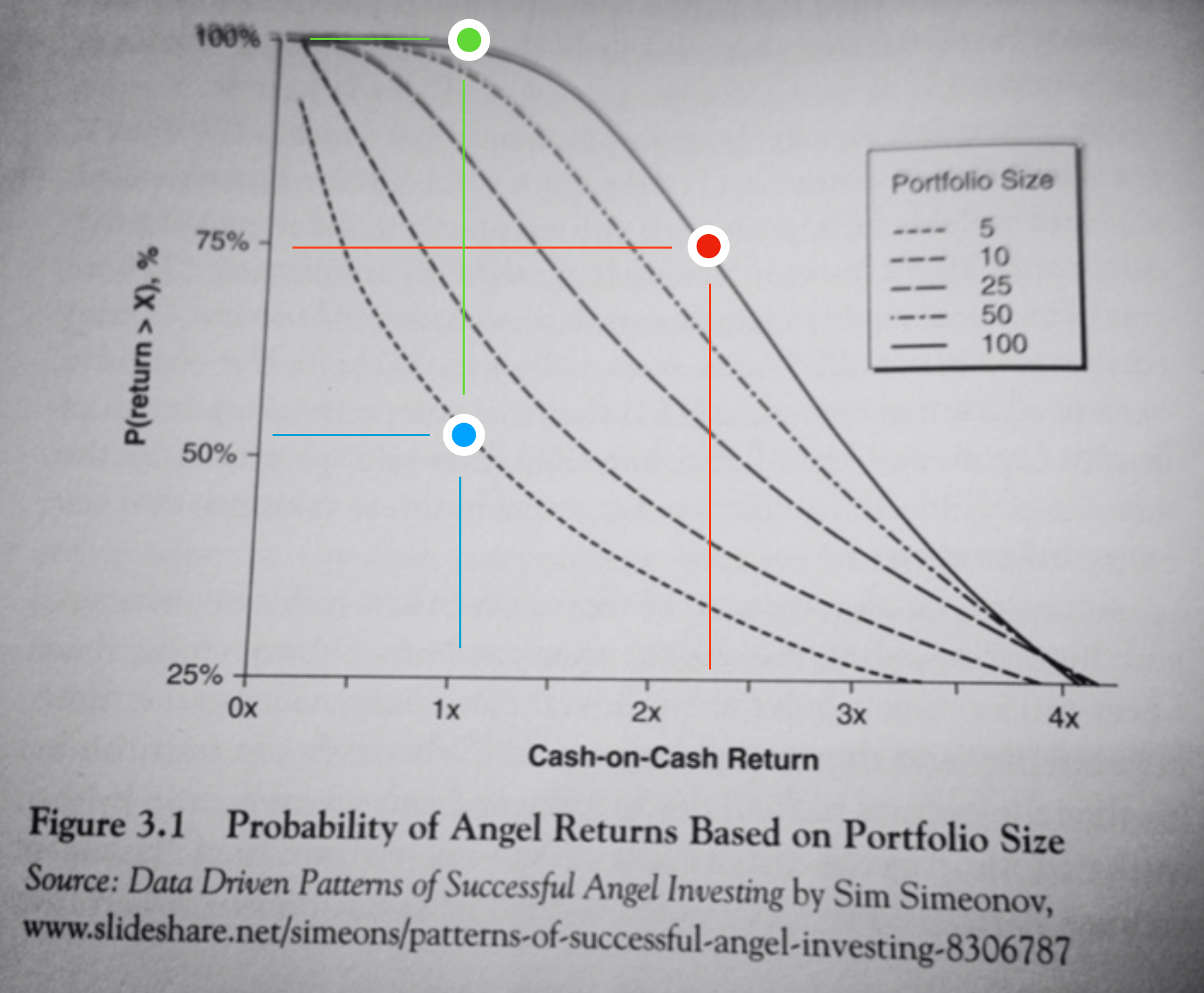

When you find studies on size vs. returns of investment portfolios, you'll always get this kind of spread:

Investing in 5 startups translates into a 50% chance of just getting your initial investment back (blue dot). With a portfolio size of 100 startups, you're pretty much guaranteed to make your money back (green dot) and have a 75% chance of more than doubling this investment (red dot).

Keep in mind this is not a law of physics but empiric research. The probabilities and portfolio size will vary depending on too many factors to account for, BUT the underlying logic is very consistent. It will apply to an innovation portfolio run by a large corporation: you need a critical size of bets to compensate for the inherent and unavoidable failure rates, create clear intermediate ROIS, and possibly two or three transformative successes after a few years.

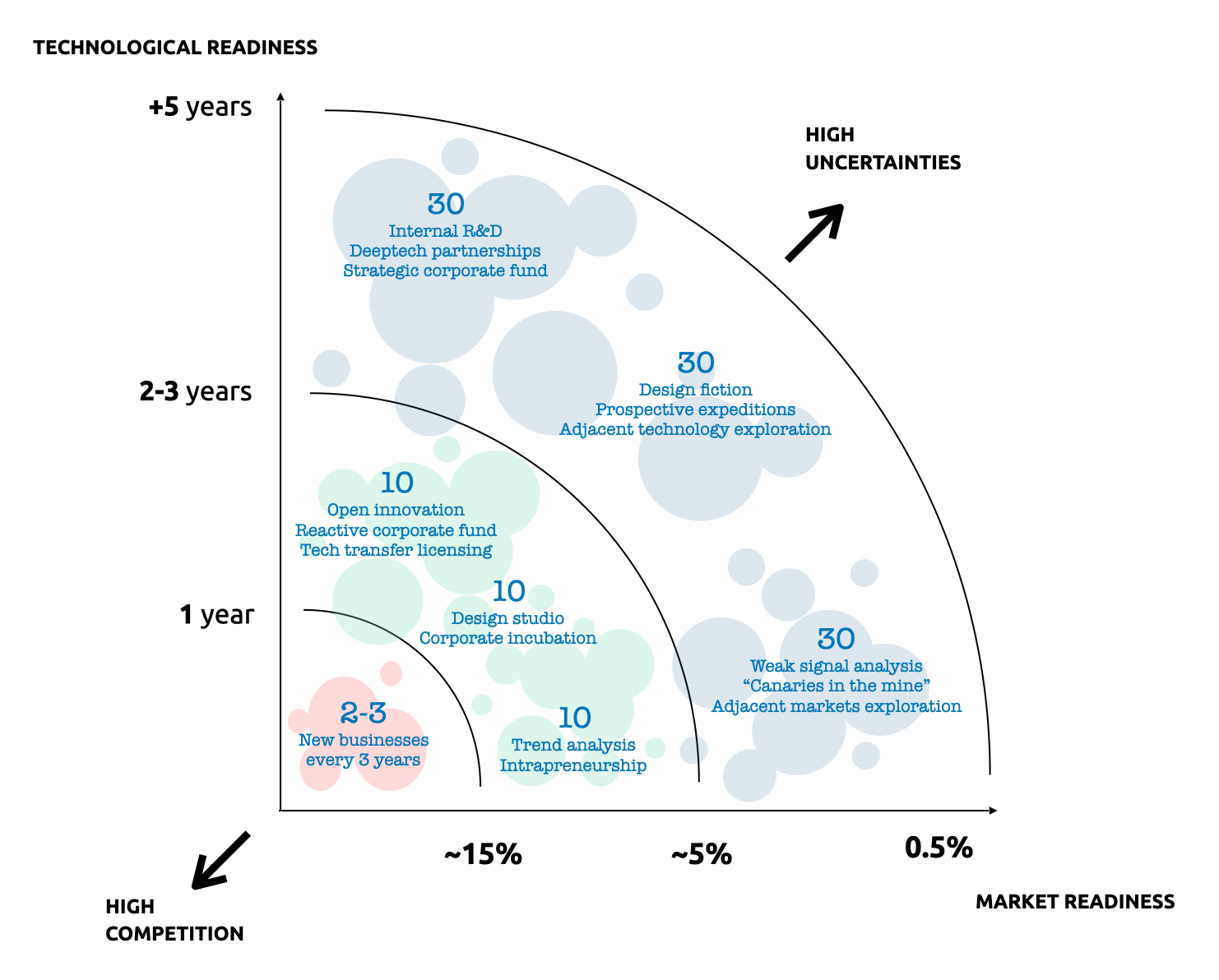

And the ballpark figure you're looking for is about 120 projects in your corporate portfolio. Not just your corporate venture capital fund but the global innovation portfolio encompassing all of your innovation processes and teams.

Something like this:

We have here a strategic spread with a simple rationale: more options on the table when there are more uncertainties to deal with, fewer options when the market starts to appear, and innovation uncertainties settle down.

There's also a qualitative aspect to this spread. Whether in a low, medium, or high uncertainty zone, we try to even out the number of projects exploring technology or market readiness. We don't choose between market pull and technology push. We play all across the board.

Optionality over serendipity

"Playing across the board," "120 projects", "strategic spread"... I'm pretty sure I can sound very smart until you start asking how can we ever afford that? The last block we need to fit all this together is indeed proper resource management.

We don't want to play on pure serendipity, which would translate to throwing projects on the wall, expecting a few to stick. No, we want to build optionality. This means that every project exploring a specific portfolio zone should be selected for minimal resource consumption and maximal potential ROI outputs.

If you have proper optionality, you can afford every single one of your projects in the portfolio to fail individually. They are designed to avoid huge sunk costs that would commit your organization to them even when they are clearly a dead end. And each one of them is also designed for delivering extremely strategic insights, unlocking a core technology that you will need no matter what, or getting a foot in a foreign market you already know you will depend on... or all of the above.

This optionality principle means that the few positive outcomes you'll accrue through the whole portfolio are so massive that they are a huge global pay-off.

When you hold an option and the world moves with you, you enjoy the benefits; when the world moves against you, you are shielded from the bad outcome since you are not obligated to do anything. Optionality is the state of enjoying possibilities without being on the hook to do anything. - Mihir A. Desai

The trick, though, is you cannot boil an egg by putting it in boiling water for ten seconds every day. Starting with only twelve projects this year and expecting to see significant (or any) ROIs won't work. You need a critical mass of projects to start with.

In Part 3 of this series, we'll explore the cultural side of things and try to map out different portfolio designs linked to the type of corporate culture you're dealing with.