So, now Apple is a bank (finally?)

In 2013, Apple launched Apple Pay as both a digital wallet and a mobile payment service, and now Apple is a bank.

Apple Pay wasn't a fantastic success even with iPhone NFC capabilities, biometric authentication, and the robust Apple ecosystem. An extra feature in Apple's ecosystem, yes, not a revolution. And since then, I've been waiting for more news and commitment to this service.

Why? Because Apple is a consumer company, payment is the key to everything's consumer.

Remember also that your single most crucial ID in Apple's ecosystem is not your face, fingerprint, or mail. It's your banking card: the first thing you need to enter to activate your iTunes / iCloud entry in Cupertino's friendly embrace.

But also because of China.

In an economy where payments are both mobile and digital, from luxury malls to street food vendors, being an actor in payment (and competing with Alipay and others) is critically important. And yet, Apple has been slow to unroll Apple Pay, market it aggressively, and use it extensively. (I'm still waiting for it in the Netherlands, where the service is unavailable for quite mysterious reasons.)

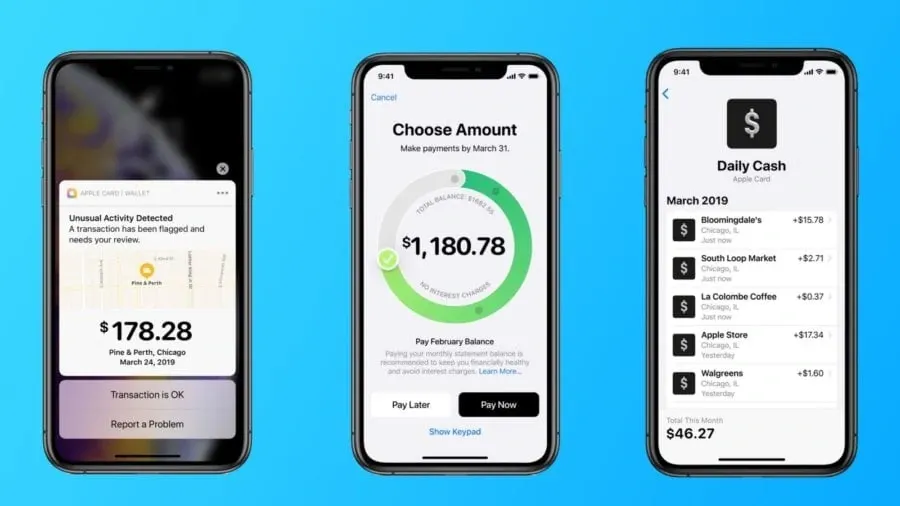

Many things were announced yesterday as a follow-up to the December catastrophic hit on Apple's market cap. All of them revolve around « more services.» That involved TV, newspapers, and… banking. Yes, a clear step up to just Apple Pay with an Apple Card and a clear emphasis: we are making a credit card designed by Apple, not a bank.

I would say that, on principle, banks (retail banks) had it coming. If Apple has been complacent in unrolling Apple Pay up to now, banks have been bloody irresponsible at letting everyone else enter their playfield, offering damn good alternatives at banking, payment, and credit for the last 5 to 6 years (check N26 success if you haven't).

Now, I'm being cautious with all this.

I believe that the days when banks dominated the retail market are just gone. Of course, Mastercard and Goldman Sachs (!) are still Apple's partners. And in that regard, Apple seems to try to be forthcoming:

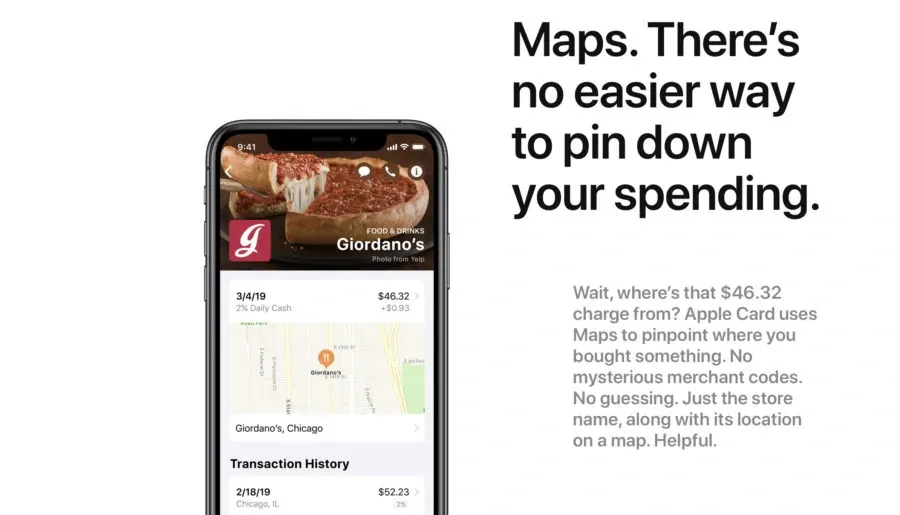

At Apple, we firmly believe in your right to privacy. That’s why we created a unique architecture for Apple Card that generates things like your transaction history and spending summaries right in the Wallet app on your iPhone. — Apple

Could we trust them to maintain high privacy standards through these incumbents? Maybe. Remember that Apple broke the music industry by partnering up with the majors when they launched the iPod, or that the iPhone was launched with AT&T? So there's that.

The core question where I'm still not convinced is how successful Apple will be at transferring its one billion customers using on a daily basis their hardware (and already with a bank account connected to iCloud) to the card.

The ease of use on mobile, frictionless integration with everything's Apple, lack of bank fees, real-time control on your budget, cash-back on purchases, … All of these are nice. But « Variable APRs range from 13.24% to 24.24% based on creditworthiness. » for the credit part?! Wow, that's very Goldman-Sachy if you ask me. And although using a banking card as a credit card (not a plain debit card) is very an American (and UK) thing, there is something wrong there. Something not wholly designed and well-thought-out?

Maybe Goldman Sachs had indeed too much to say about it, but maybe (and I'm trying to be optimistic) it's a temporary thing. Remember that Apple rarely gets its first version of a product right or « complete.» The iPhone was launched without the App Store, and more recently, it took several iterations before the iWatch was jelled as a health/fitness device.

So we will see how fast they unroll their card and how far they intend to go. But I will say that how they will adapt it to China's payment needs will be set to watch very closely from now on.

An interview on CNBC seems to indicate that, yes, they're going for it…

“With that product (Apple Card) we are going to start in the U.S. but over time, absolutely, we will be thinking of international opportunities for it.” — Richard Gnodde, CEO Goldman Sachs

Keep in mind, though, that it's not Tim COOK committing to this yet…