Gauging a market innovation dynamism

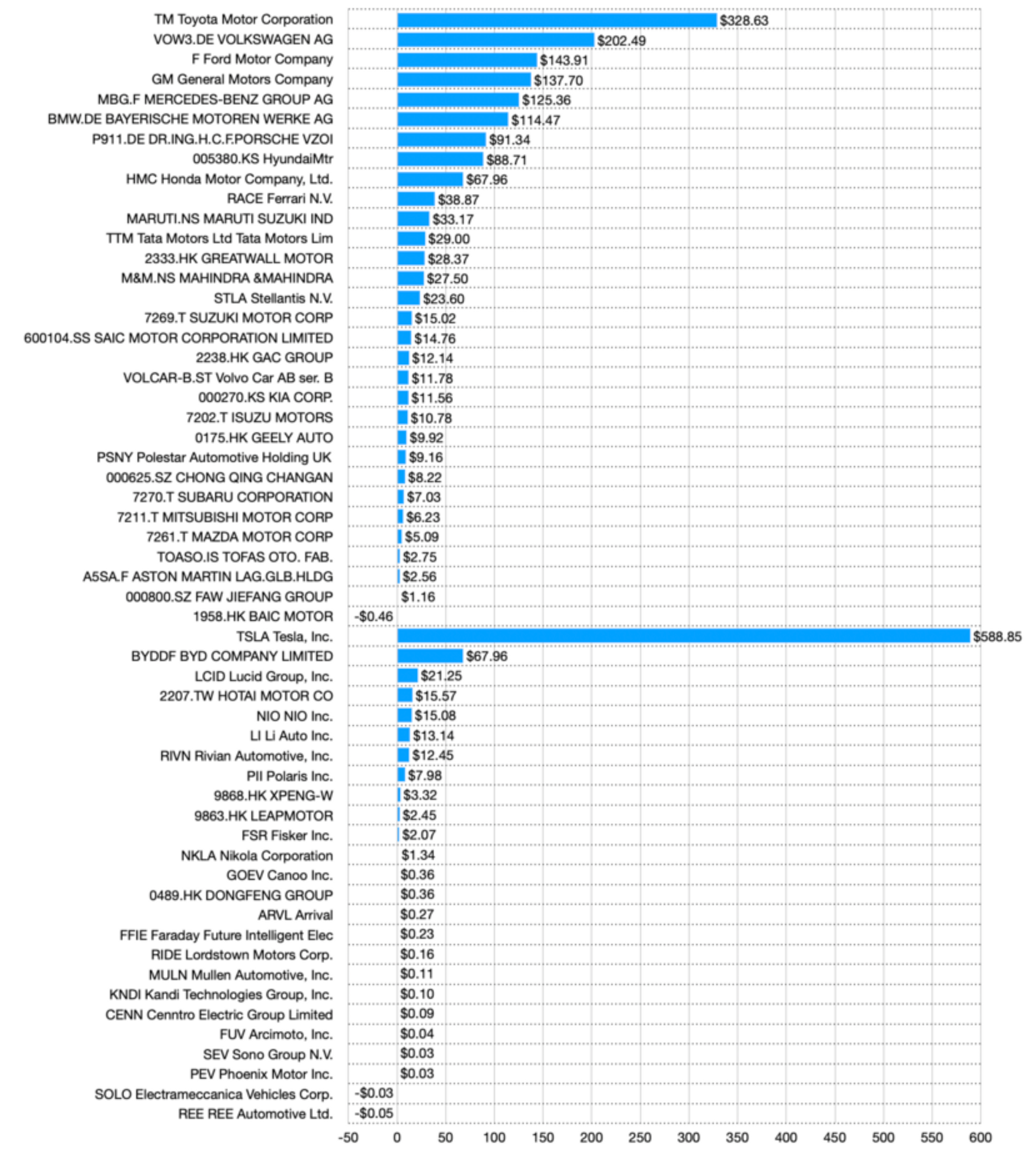

A recent article from Horace Dediu (analyst extraordinaire) caught my eye recently. It crunched the numbers on what is the enterprise value of automotive companies worldwide in terms of 25 new entrants (<20 years old) and 31 incumbents, as reported by the OICA (International Organization of Motor Vehicle Manufacturers).

The enterprise value is an interesting indicator as it is the company's market capitalization minus cash plus debt. As a sector that relies heavily on debt financing, it's a better indication of the future value and non-liquid assets of the companies (better than, say, the number of cars sold or just the market capitalization). Also, it's a better indicator than 'vehicles sold' because many of these companies have a range of micromobility vehicles (devices?) that are usually not counted as vehicles.

The result is as such:

If you want to gauge the innovation dynamism of this sector, the enterprise value is only a partial indicator for sure. I'd argue, though, that it might be better than most other ones:

- R&D spending, although a get-go innovation indicator, in practice, is a very poor one. Incumbents, while they over-invest with public money sponsoring and consequent tax breaks, don't deliver much. And they tend to rely on Tier 1 and 2 subcontractors to do the innovation heavy lifting. New entrants, on the other side, do transform much more R&D spending into effective innovation but tend to be more frugal.

- Vehicle sales don't tell much about innovation unless you'd be willing to go into details about the different categories and distinguish, say, electric vehicles with some self-driving capabilities from gas vehicles. But still, is that innovation?

- Startup investments and collaborations could be interesting to some extent but are only very partial indicators poorly correlated to innovation success (at best). And in any case, they rarely apply to new entrants.

All in all, in a market where turnarounds happen only after five to ten years (Tesla was founded in 2003 😱), the enterprise value gives an overall fair directionality assessment.

So what do we learn from it?

- The incumbents still weigh $1.6 trillion vs. "only" $753 billion for the entrants. This means that the automotive market is indeed past a tipping point and now transitioning to a new crop of actors. How fast the enterprise value of the new entrants will grow will map out how fast this transition happens – and, again, in such a slow market, it's an easy indicator to monitor.

- The new entrants are largely Chinese and Indians. No surprise here, and more to come as the U.S. (soon Europe, too) will find new reasons to apply tariffs or tax penalties to foreign companies destabilizing home-grown incumbents. The keyword for the next decade will be protectionism.

- Except that the largest enterprise value of the new entrant's category is still Tesla, weighing 75% of the total value in this group (Lucid Motors is only at 3%, Rivian at 2%). This is an alarming indication of how very few new companies have managed to seize a significant market foothold and how fragile innovation is in this sector.

- All this doesn't factor in market outsiders such as Amazon, Google, or Foxconn that are aggressively seizing the digital layer (which, eventually, will be the most important one).

This quick discussion certainly shows how difficult it is to define innovation and, even worse, try to gauge it. At best, this is about finding reasonable proxies.