While startups are not failing more, they’re just more vocal about it. This is a good thing. Hopefully, it will hep dismiss the illusion that a) anyone can launch a successful startup and b) the next stage of economic growth for Western countries will come from under-staffed, ill-prepared tech entrepreneurs.

Startups being half of my daytime work and I deeply care about them. This often makes me vocal on how entrepreneurs are abused in launching projects that only fuel tax exemption of unconcerned investors, or the regional marketing of cities despairing to rebuild territorial attractiveness.

The startup game

When I train entrepreneurs, one of the key discussion we always have is: how much risk they’re going to leverage.

This is always rather uncomfortable at first. But clearly, if you want to sort startups that have a chance to survive from sitting ducks, asking: “What is the nature of the risk you’re taking?” is a powerful tool.

Now, the question is tough. It is a least a two-fold question and an extremely technical one at that. However you want to answer it, it’s about a) the level of technical and market readiness of the ecosystem around what you want to achieve and b) how far your project anticipates the future evolution of said ecosystem.

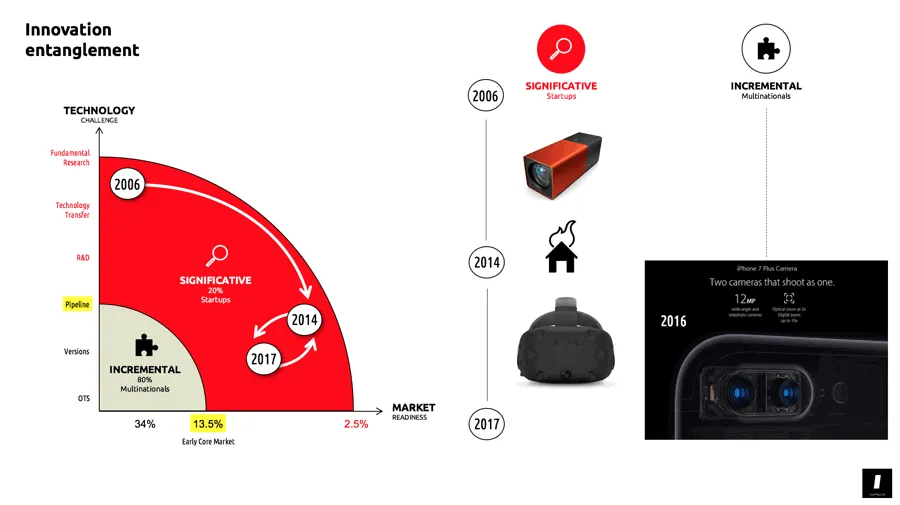

When in 2006, Lytro set sails to discover a future market before they ran out of money, they were rather lucid regarding the risk they –and mainly, others– were investing in:

With Lytro I’d embarked on a new kind of challenge — that of a “hard tech startup.” These are companies where, at the outset, you don’t know whether the core tech needed for your invention will work at all. The forces of physics, biology, and Moore’s Law can bedevil you in unexpected ways. Building a winning product is already challenging enough; with hard tech startups, the obstacles are even greater.Jason Rosenthal, CEO Lytro

As far as I’m concerned, this is not so much about “hard tech startups,” it’s about all startups.

The so-called hard tech ones are only focusing on pushing technology to the market. It has to be technically very challenging. If it’s not, then anyone could do it. And by anyone, I mean a much more robust player in the optic/image market such as Zeiss, Leica, Nikon, or… Nvidia.

For startups, risk is the principal barrier to entry. It’s often the only one.

So, for Lytro risk was essentially about technology, and they were starting from a very high-risk zone. They didn’t want to make better lenses or new digital sensors, things that the market already knew and was using, they wanted to reinvent how pictures were taken, by allowing a full post-processing of depth of field.

It was a big deal if they succeeded.

Or was it? In a few years, Lytro had to face a rude awakening: their technology was remarkable (and they managed to build it), but no one cared enough to buy it. This lead Lytro to scrap their plan of inventing a technology that the market will beg for, to find a market that would care (VR):

We’ll see where this startup is going from there on. But I wouldn’t be very optimistic: this startup doesn’t get risk as a key driver of their project. Why would I say such a horrible thing? Because the Rosenthal’s quote you read just a few paragraphs before, is not from 2006, it’s from last week.

That means that this startup initially thought they were pushing a technology that was very risky to try to develop, to a market that was ready for it. Nope, there was no market. Or the market was not there yet, or the market didn’t like the way it was done… So what they did is that they changed the nature of the risk they were trying to leverage. Now that the technology was there, they’re trying to push it to a market that is clearly not there yet. VR being at hype’s peak right now, there couldn’t be a more volatile choice to make regarding who’s going to buy.

And yet, Rosenthal still believes it’s about hard tech. No, it’s not. Not anymore. It was in 2006, but now the tech is here, so it should be about building a company around customer intimacy and design, not engineering again.

Eventually, when the startup waits too long multinationals appear and bring together innovation as an incremental step. The window of opportunity is gone:

Despite my concerns, I do hope that Lytro will pull it off. The tech is really a potential game changer. I just suspect they didn’t focus yet on what added value they have, and since I’m not an advisor, I will not push that further (oh well… coughdestructive testingcough).

But as with any startup, risk is key to strategy.

Valuation and the nature of risk

Risk is also what justifies “insane” exit valuations. Create a startup that helps a few dozen retail shops in your region to sell more online, and you’ll be able to buy a new German car next year. Change the way ads are managed and paid for online in Europe and the US, and you can buy a German car manufacturer in five years.

Understand, that the risks that startups take are not theoretical. They are benchmarked in regard to what the current multinational leaders of the playfield can achieve. Any decent startup will try to do something at least slightly difficult (to completely impossible) for such multinationals.

That is why the higher risk you start with, the higher the financial leverage you’ll make on your equity.

That is also why more than 90% of startups crash. Because they’re doing things already difficult for multinationals. And if they don’t, they’re not even startups; they will be rolled over by Amazon, Google or anyone big shifting slightly their current offer.

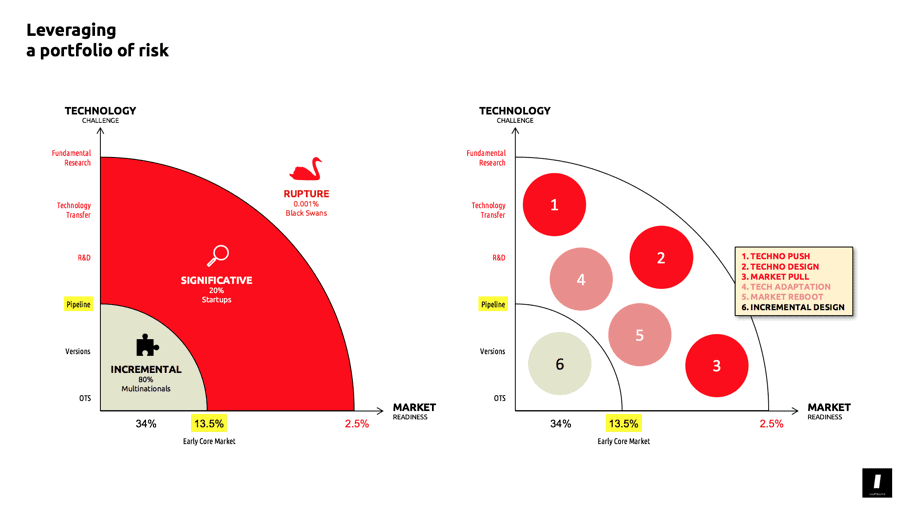

Eventually, if you shift your perspective from a startup at a time, to the whole playfield, you’ll map something like that:

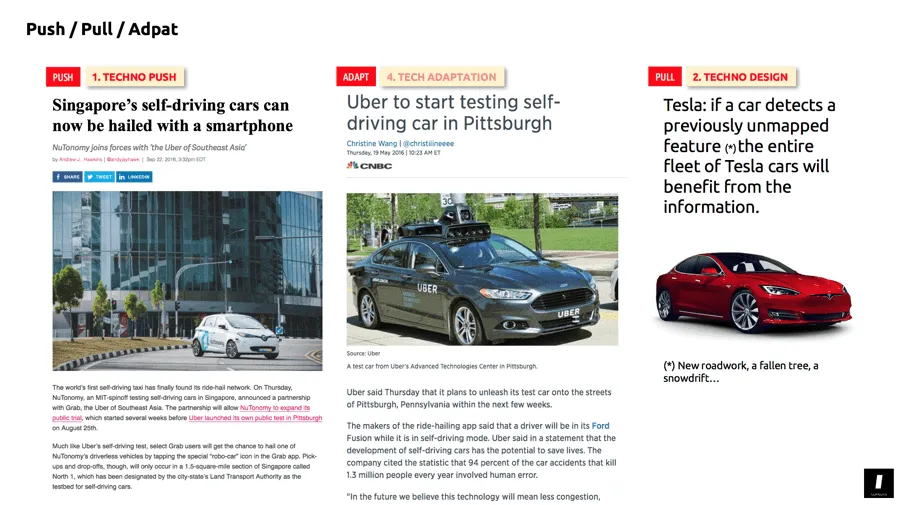

To innovate the market, some startups prefer to build breakthrough tech and push it for a market that is already asking for it (1). It’s for instance, the whole story of biotech startups. You think you can cure cancer? Don’t waste time on figuring out marketing segmentation and business model, just lock yourself back in your lab.

But you can also decide to bring mobile payment solutions for retail shops in Europe, and that would be a totally different ball game (3).

Focus on a single playfield/market and check who’s trying to innovate it? You can easily cluster them by the nature of risk they’re taking:

But also by how much risk they’re taking:

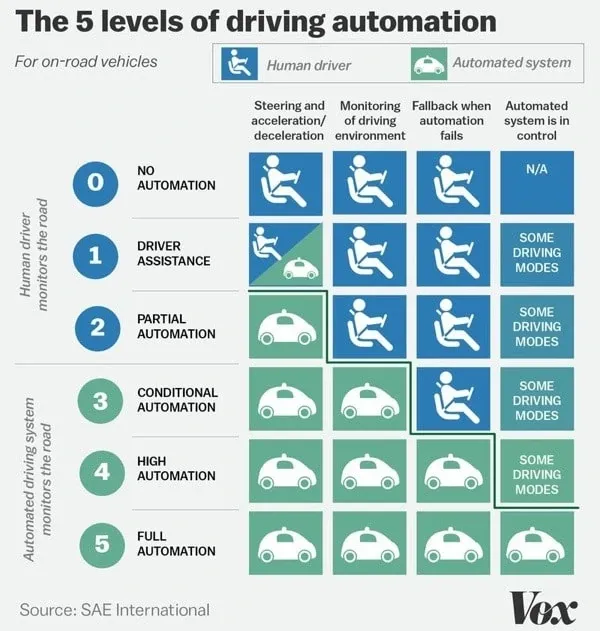

Depending on what you want to achieve from 1 to 5, it not only means that the tech risk will be higher but also the market risk (by now you get the narrative “Who’s going to be responsible when a driverless car kills a pedestrian?”).

To say it again: as a startup help Volvo and a few others dramatically enhance their Lidar to deliver exceptional level 1 features for their 2017-18 high-end cars, and one of them will eventually buy you out. But if you manage to sell by yourself a few thousand level 5 self-driving cars this year, you might the one buying out car manufacturers.

Why? Because while the first scenario is reasonable, the second one is insane. Pull it off, and you get corresponding “insane” valuation. Mathematically.

In the end, any major innovation like changing the way we commute and travel never happens in a linear way. It’s about a flurry of small dents in the market, a lot of big punches into it, and rare but decisive thermonuclear events.

The metagame

In all this, we only considered the perspective of a single startup or a collection of startups aiming to innovate a market ecosystem. But what if we decided to be statistically sure enough to know who’s going to win the innovation game?

How to crack the problem of finding which startup will win the game?

In my experience, you only have two answers: black magic and playing power laws. My personal knowledge and affinity with black magic being rather limited, I’d stick to what I know.

VCs understood a long time ago that if you want to invest in the startup which will eventually reinvent the mobility market, no one is “smart” or visionary enough to pick the one three to five years before everyone else. And apparently, they’re not fond of black magic either.

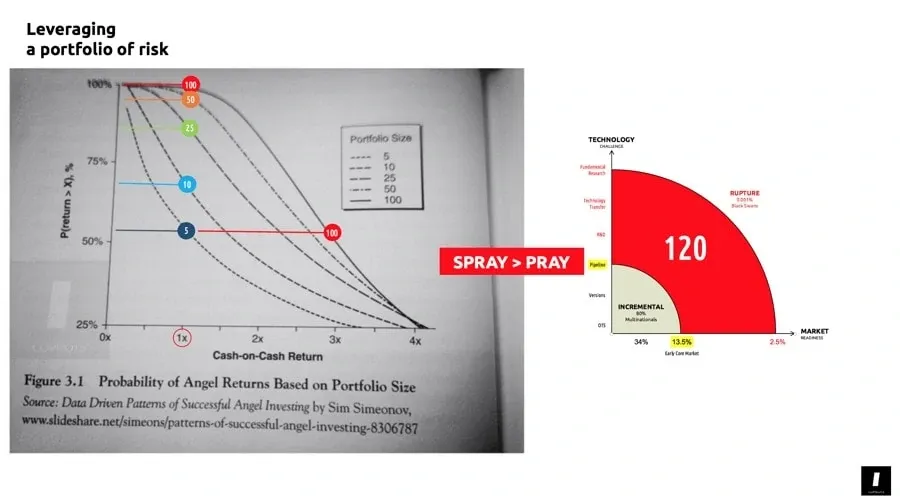

The innovation meta-game is not about intelligence, experience or education. It’s about playing at a scale just large enough to guarantee an acceptable outcome, and maybe once every three years, a big score.

I find it entertaining (and well, somehow profitable if I must say) that not many industrials caught up with this very well-known power law:

We spoke of it many times when discussing corporate incubation. It’s everything but a secret. But as far as multinationals are concerned, an Innovation SVP selling to an executive committee that investing in a dozen startup a year won’t cut it (not before 10 or 12 years) is in a tough spot.

For the industry, the real difficulty is not about the mathematics (if we dare call that empirical –but stubborn– power law mathematics). The difficulty is on how to achieve 120 startups incubated over a two to three years period.

If there are many techniques and ways to engineer such volume, the starting point tough for consultants as ourselves is to detect companies which have skin in the innovation game. Most multinationals are content with road trips to San Francisco or invite press when they redecorate funky open spaces and fab labs.

The biggest meta-game of all though is played at a national level.

And this is for me an even bleaker picture than what occurs at companies’ level. The reason is that most European countries are only focused on pushing public research to complacent markets. It’s not that it’s the worst kind of risk to leverage, it’s that you don’t build whole innovation ecosystems on a unique principle.

Selecting startups through tech transfer based on their IP has been producing generations of rock stars. Rock star engineers, alas, not entrepreneurs. And while Europe steadily became a technical sweatshop for the rest of the world, every niche of our economy is now occupied by Google, Amazon,… and soon Baidu or Tencent.

In the innovation playfield, being just “smart” is an unforgivable error. We’ve been paying for it dearly at every level. It would be nice to collectively wake up and start to play by the numbers.